|

|

Post by FD1000 on Aug 25, 2021 16:27:30 GMT

I would still consolidate into max 2 discount brokers. My favorites are Schwab+Fidelity, unless you believe in VG funds and want to own the Admiral shares. I just received the Semi Annual Report dated 06/30/2021 for T. Rowe Price Capital Appreciation Fund ( link). Giroux is one of my favorite managers if all time. From the link.

Now I will remind our shareholders we are not economists. We don’t have GDP forecasts. We don’t design our portfolio based on a macroeconomic viewpoint. The history of the last 20 years is one of mean reversion of economies. When things feel bad (as they did in March of 2020), they tend to feel very good one year later (as they do now) and vice versa. When the macroeconomic consensus is positive, we tend to be a little more conservative, as we are now. When the macroeconomic consensus is negative, we tend to be more aggressive, as we were in March of 2020, December of 2018, September of 2011, and early in 2009. Taking the other side of the macroeconomic consensus has created substantial value for our shareholders over the long term.

Our equities underperformed the S&P 500 by 41 basis points (14.84% versus 15.25%) during the first half of 2021. However, over the last 1-, 3-, 5-, and 10-year periods, our equities have outperformed the S&P 500 by an average of 294, 505, 317, and 452 basis points annualized, respectively. Our fixed income investments outperformed the Bloomberg Barclays U.S. Aggregate Bond Index by 425 basis points (2.65% versus -1.6%) in the first half of the year. Interest rates rose during the first half and this caused losses in traditional fixed income investments. Our fixed income investments rose in value as we hold primarily high-quality high yield and leveraged loans with very low duration, which should do well if rates increase.

For the 1-, 3-, 5-, and 10-year periods ended June 30, 2021, we outperformed our Lipper and Morningstar peers over every period, except the last year, in which we are at the 50th percentile in Lipper. The Lipper peers tend to have substantially higher equity weights than the Capital Appreciation Fund and Morningstar and, in strong market environments, this can be a difficult challenge to overcome. However, over the last 10 years and also over the last 15 years since the current portfolio manager took over the fund in 2006, we are in the first percentile in both peer groupings. (Based on cumulative total return, the Capital Appreciation Fund ranked 224 of 454, 6 of 433, 11 of 408, and 1 of 291 funds in the Lipper mixed-asset target allocation growth funds universe for the 1-, 3-, 5-, and 10-year periods ended June 30, 2021, respectively. Results may vary for other periods. Past performance cannot guarantee future results.)

|

|

dirk

Ensign

Posts: 42

|

Post by dirk on Aug 25, 2021 20:45:23 GMT

I would still consolidate into max 2 discount brokers. My favorites are Schwab+Fidelity, unless you believe in VG funds and want to own the Admiral shares. You kinda nailed it, FD. We've had Fidelity since the early 1990s for my wife's IRA alone. This past year, we toggled over to their broker platform and expanded to three accounts: her T-IRA, my Roth IRA (individual stocks), and our joint brokerage (also individual stocks, natch). I will have some money from a small corporation I've long held (active since 1983, in mothballs since c.1996) but will shut down soon, plus some joint savings that will also end up here. Fidelity having a bricks-and-mortar location here in San Antonio was a deciding factor: easier for my wife to deal with someone in person to sort things out if I'm gone. However, Vanguard was always our go-to - again since the early 1990s - for our joint taxable investments: money market fund (with checkwriting) + several equity funds (most Admiral class). We also had to transition to their broker platform about a year and a half ago...at Vanguard's insistence (can't say I was that happy about the change, but I'm resigned to it). For a while, a few years back, their phone reps left a LOT to be desired, but seem to have improved more recently. I like the low fees too, but honestly, I'd consider taking these assets elsewhere if exposing the holdings to LT cap gains/taxes weren't so problematic. But I've heard too many less-than-fun reports of trying to send them as is to Fido, even for simple housekeeping purposes. T. Rowe Price holds two accounts: my T-IRA (PRWCX, PRNHX, PRGTX) and our only non-joint taxable holdings, the proceeds of my dad's estate (PRWCX, PRIDX, PRMTX). Once (1) my wife actually retires and (2) I'm satisfied with the allocation between funds at that moment, I'll likely keep the funds but sweep the holdings over to Fidelity, as well, just for housekeeping simplicity. I like TRP's reps best of all three houses in terms of friendly and helpful service by phone, but their brokerage side has almost no reputation (and what I HAVE heard ain't all that impressive)...otherwise staying put here might be more attractive. FWIW, I checked out Schwab pre-pandemic (they have a physical office here too, though still not open full-time now due to health protocols) but was less than blown away by the people I interfaced with. Kind of a snooty element that took me aback and that I know would not fly with my wife. I confess that I already miss TD Ameritrade, my former broker (since their TD Waterhouse days) and a place I migrated away from simply because their future as a...what, part of? partner of? disappearing entity? offshoot of Schwab...seemed too uncertain. What I said about T. Rowe phone reps being the best? I'd put TD's phone reps on the same level if not higher. But I'm not going to put my wife at the mercy of that kind of uncertainty. Thus the choices I made for the final three: Fido, VG and TRP. Dirk |

|

|

|

Post by nobhead on Aug 26, 2021 2:28:22 GMT

jongaltiii , dirk , My spouse has PRWCX in personal non-IRA account at Vanguard. I also have a non-IRA personal account at Vanguard. I think she can gift me shares but the question is, can I add shares to it after it has been gifted?

TIA Nob

Hi Nob. Short answer: don't know...it's a question for T. Rowe. Also possibly Vanguard. Holding shares of one company's mutual fund at a different mutual fund company or broker? It often involves added fees or convoluted rules about access/additions (on both sides) that either confuse me or annoy the heck out of me. Over the years, I've noted major examples of "turf-fight silliness" about Vanguard funds held at Fidelity and vice versa. T. Rowe doesn't seem as crazy, but we're also talking about access to a closed fund here, and as I note...their fund, their rules. Get them to explain. This is one of the reasons I edited the post above to emphasize that, if you're doing my suggested back door (401k rollover -> new IRA invested in PRWCX), you expect to hold and grow the IRA at T. Rowe and keep it there until you understand all THEIR rules about what you can and can't do. However, if your spouse owns PRWCX in a taxable account, I'm sure gifting of shares is possible. But my first question would be...are you keeping all your finances separate for reasons of personal independence? Maybe a prenup agreement? Or because she inherited the account and needs to keep the funds isolated from shared ownership (say, to protect them from legal attack if you are sued)? Yes, these ARE valid reasons to keep things separate. But assuming they don't apply to your personal situation, consider talking to your spouse about redesignating her Vanguard taxable account as Joint Tenancy with Right of Survivorship. This makes you a co-equal owner and allows you to add to or withdraw funds from PRWCX (again, according to the rules set out by Vanguard and T. Rowe). Ergo, no "gifting" of shares required. (Also gives the survivor continuous access to the funds, before and during probate of any will...my wife and I have all our joint holdings designated JTWROS.) Remember, too, that PRWCX isn't exactly ideal for taxable investments...better for tax-advantaged (IRA, SEP, 401k if available) accounts. Yes, I was being tax-silly when I invested taxable money in it back in 2004 or so -- read my long post again. Consider that aspect before you jump through a lot of gifting and transfer hoops. Just sayin'. If you want PRWCX as an IRA (solo or component) fund, the rollover backdoor is so-o-o-o much easier. Good luck, however you decide to proceed. Dirk |

|

|

|

Post by chang on Aug 26, 2021 2:55:04 GMT

Mileage varies. I found Schwab to be slow, unresponsive, unhelpful, and expensive. Took my $2500 promo for a TOA and left after a year. Been with Fido since 1985, and they've always been [nearly] perfect. I recently TOA'd for a $2000 promo and they gave me $2500 just to be nice. TDA had the best customer service of all, but I consolidated to Fido and VG for simplicity. Two brokerages is enough.

|

|

|

|

Post by jongaltiii on Aug 27, 2021 23:15:07 GMT

There’s probably nothing profound about this observation… With that disclaimer, I was taking a closer look at FMSDX vs PRWCX and FBALX and performance-wise… I’m not dissatisfied with how FMSDX and FBALX are performing over the last 1-3-5-10 years. In fact, been pretty happy with how FMSDX is doing and they all have similar ER.

YTD/ 1 yr / 3yr / 5yr /10yr

PRWCX: 13.57 / 26.15 / 16.62 / 14.07 / 13.10

FMSDX: 13.56 / 27.01 / 16.51 / 11.35

FBALX: 13.44 / 28.71 / 15.87 / 14.18 / 11.65

|

|

dirk

Ensign

Posts: 42

|

Post by dirk on Aug 29, 2021 21:02:29 GMT

I was taking a closer look at FMSDX vs PRWCX and FBALX and performance-wise… I’m not dissatisfied with how FMSDX and FBALX are performing over the last 1-3-5-10 years. In fact, been pretty happy with how FMSDX is doing and they all have similar ER. Your call on whether you stay put with current holdings or add PRWCX to your IRA quiver, jongaltiii. At least you know how to get in if you want to. As for performance, we'll see how Giroux handles the next downturn. I love how he built up dry powder and snatched up bargains last year. It appears that he's getting ready for more turbulence. Dirk |

|

|

|

Post by shipwreckedandalone on Sept 1, 2021 14:42:30 GMT

Did PRWCX reduce equity exposure allocations pre Oct 2007?

|

|

dirk

Ensign

Posts: 42

|

Post by dirk on Sept 1, 2021 17:13:09 GMT

Did PRWCX reduce equity exposure allocations pre Oct 2007? Not positive but maybe John Taylor recalls. I was kinda crumpled in a little ball whimpering in the corner of the room during much of the massive downdraft period (never sold any holdings but it was definitely a scary time)…also I didn’t buy many investing periodicals during the time, so it isn’t well represented in my archives. I do recall that PRWCX was one of the first funds to show significant signs of recovery in my portfolio, so maybe so. Do remember that Giroux had only been on board for a year or so, even though the “build up cash” tradition was already established with previous managers. Dirk |

|

|

|

Post by yogibearbull on Sept 1, 2021 22:23:35 GMT

|

|

|

|

Post by FD1000 on Sept 13, 2021 12:54:00 GMT

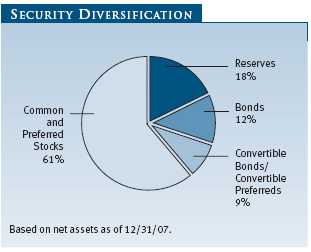

When I looked at Trow site ( link), PRWCX stocks % is close to 70% as of 8/31/2021. Attachments:

|

|

|

|

Post by yogibearbull on Sept 13, 2021 14:44:30 GMT

M* shows 69.94% equity as of 6/30/21 and Price website shows 69.80% as of 8/31/21. So, I don't know what were the mentions of reducing equity % in media (there were multiple reports) were all about? May be Giroux changed his mind but the stuff in print remains.

|

|

|

|

Post by johntaylor on Sept 26, 2021 17:52:03 GMT

In 2006, T Rowe credit analyst Susan Troll began telling managers to ditch subprime and thankfully they listened.

That helped many funds.

TR's AUM did drop in Crash of 08, but it had zero debt and was hiring.

|

|

|

|

Post by shipwreckedandalone on Oct 9, 2021 14:59:15 GMT

PRWCX performance since 9/2 compared to other funds on my watch list has been in obvious risk off mode.

This thread discussion has focused on equity asset allocation % vs historic. I would suggest to focus attention on the valuation/beta/aggressiveness of the individual stocks held within the 69% equity portfolio as of 9/30 update vs 8/30 seen on their website.

|

|

dirk

Ensign

Posts: 42

|

Post by dirk on Oct 23, 2021 16:41:56 GMT

A person named cmurdock with, apparently, far greater internet search skills (and patience) than I, has posted on M* and given us an answer to the question posed much earlier in this thread: who was the first (original) manager of PRWCX? With links to verification, no less. Thank you, cmurdock! I reprint your reply below for Big Bang readers. Cheers, Dirk

Richard Fontaine - original PRWCX manager www.washingtonpost.com/archive/business/1988/03/14/t-rowe-price-fund-manager-buys-stocks-others-wont-touch/c00ecb53-565a-4a69-92e0-779529f2012d/ The primary goal of a capital appreciation fund, as its name suggests, is to make an investor's money multiply as fast as possible. The funds are intended for long-term investors willing to accept the extra risks that go with an aggressive approach. The fund was started by Fontaine, who has been with T. Rowe Price since 1981. He came to the firm with six years experience as a computer salesman for International Business Machines and an MBA from Harvard University. As a contrarian, Fontaine often buys stocks few other investors will touch. Hang crepe on a once-popular company and Fontaine will take it into his heart and into his portfolio. __________________________________________________________________________________________________________________________________ za.investing.com/funds/t.-rowe-price-capital-appreciationa-company-profile Vice President, Portfolio Manager 1986 1989 In January 1989, Fontaine became president and chief investment officer of Richard Fontaine Associates. He served as a vice president and investment manager at T. Rowe Price Associates from 1981 to 1988. As a portfolio manager, he seeks capital appreciation based on four tenets: valuation, contrary thinking, opportunistic execution, and preservation of principal. Fontaine has completed NASD Series 7, 26, 63, and 65. Born June 29, 1951 in Westerly, Rhode Island, he has four children. |

|

dirk

Ensign

Posts: 42

|

Post by dirk on Oct 26, 2021 17:12:10 GMT

Per the announcement by TRP concerning "Summit" benefits (basically, if you have $250K or more invested directly with them...that is, not through a third party), so-called "closed" funds will be open to you as of November 15. If you've been wanting into PRWCX and haven't wanted to do the backdoor 401(k) -> Rollover IRA route, this could be your chance. Also, expenses will be reduced. Details at www.troweprice.com/personal-investing/campaign/summit-program.html?van=summitFWIW, Dirk |

|

|

|

Post by johntaylor on Nov 2, 2021 13:38:08 GMT

More on the dawn of Cap Apprec Fund: www.baltimoresun.com/news/bs-xpm-2006-02-12-0602110032-story.html"Richard Fontaine, who started the Capital Appreciation Fund, said the market was "insane" and suspected that stocks were overheated. He reacted by stashing 80 percent of the fund into cash holdings shortly before the crash, and shortly afterward he bought up downtrodden stocks. Fontaine, who now runs a small investment firm in Baltimore, said he had designed the fund to give managers maximum latitude "to get out of the way" of severe market swings. Since then, the fund's charter has been rewritten to require that at least half of its assets are invested in stocks..." |

|

|

|

Post by johntaylor on Nov 6, 2021 0:47:59 GMT

So the mgrs were Richard Fontaine (Harvard MBA), Rich Howard, Steve Boesel (sgt in VIetnam and Colorado MBA), Giroux

|

|