|

|

Post by xray on Nov 5, 2023 20:35:19 GMT

GOBankingRates

How Much Money Should You Have in the Stock Market if You’re 75?

Vance Cariaga

Sat, November 4, 2023, 2:00 PM EDT·3 min read

Conventional wisdom holds that when you hit your 70s, you should adjust your investment portfolio so it leans heavily toward low-risk bonds and cash accounts and away from higher-risk stocks and mutual funds. That strategy still has merit, according to many financial advisors. But with people living longer, you should devote a higher proportion of your portfolio to stocks now than seniors 30 or 40 years ago.

Many older Americans are following that advice. As The Street reported earlier this year, among older seniors with taxable brokerage accounts at Vanguard, nearly one-quarter of those aged 75 to 84 had nearly a 100% weighting in stocks. Even one-fifth of investors 85 and older had a similar weighting in stocks.

Mick Heyman, an independent financial advisor in San Diego, told The Street that one reason older investors are keeping more money in stocks these days is to avoid capital gains taxes for selling them (assuming that they are in non-retirement accounts).

“If you originally had 60% to 70% of your assets in stocks, maybe you’re now at 70% to 80%,” he said.

As for why many older investors are investing more in stocks, much of that has to do with income — an important consideration for those who expect to live a long time in retirement.

“The most important thing is income,” Heyman said “Do you have enough based on your allocation and the potential volatility in stocks to finance your spending if you live as long as possible?”

Also: 5 Places to Retire That Are Just Like Hawaii but Way Cheaper

Americans Living Longer, Meaning Retirement Investment Mixes Have Changed

In terms of how much money you should have in the stock market at age 75: That depends on several different factors, ranging from your health and preferred lifestyle to your debt load, net worth, monthly bills, income sources and risk tolerance.

One old bit of general wisdom cited by CNN is that you should subtract your age from 100 to come up with the percentage of your portfolio that should be in stocks. If you’re 75, for example, then you should have 25% in stocks.

But now that Americans are living longer, that formula has changed to 110 or 120 minus your age — meaning that if you’re 75, you should have 35% to 45% of your portfolio in stocks. Using this formula, if your portfolio totals $100,000, then you should have no less than $35,000 in stocks and no more than $45,000.

According to a recent analysis from Empower, a financial services company, investors in their 70s and over keep between 31% and 33% of their portfolio assets in U.S. stocks and between 5% and 7% in international stocks. Among the investors that Empower analyzed, here’s the breakdown by age group based on average holdings:

Age

U.S. stocks

International stocks

70s

$247,645

$39,774

80s

$196,042

$24,795

90s

$145,292

$13,183

In terms of bond holdings as a percentage of their overall portfolio, here’s how older investors break down:

Age

U.S. bonds

International bonds

70s

11.39%

2.04%

80s

11.05%

1.81%

90s

9.97%

1.32%

Like most investors, seniors tend to have less money in alternative investments. Here’s a looks at the money older investors have in alternative investments and their percentage of the overall portfolio.

Age

Median allocation of alternatives

Pct. of alternatives in overall portfolio

70s

$14,361

3.74%

80s

$8,773

3.48%

90s

$4,228

3.17%

----------

Live Long and Prosper....

|

|

Deleted

Deleted Member

Posts: 0

|

Post by Deleted on Nov 6, 2023 1:23:03 GMT

I suggest another contributor to us elderlies having a high percentage in equities is that we are the last generation likely to have generous private pensions. The income allows considerably more investing options.

|

|

|

|

Post by gman57 on Nov 6, 2023 1:58:42 GMT

I've been reading lately. Reduce equities slowly from retirement or maybe a little before until about 80. I like the 120-your age in stocks. Then once you hit 80 if you have enough for yourself start increasing your equity holdings again since you're probably investing for your heirs.

|

|

|

|

Post by catdog on Nov 6, 2023 2:59:52 GMT

Keep as much in equities as you can stomach. By 75 your crystal ball should be pretty clear (maybe the mind is getting cloudy). By no means should you go lower than 40%. That leaves quite a bit for income

catdog

|

|

|

|

Post by Mustang on Nov 6, 2023 5:51:36 GMT

There are multiple theories. Bengen's research, as well as others, indicate that stocks should be as close to 75% as possible and never less than 50% for basically all withdrawal periods from 15 years to 40 years. The FIRE (Financial Independence Retire Early) investors believe that for early retirement stocks need to be 80% to support a longer payout period. Then there is the declining allocation theory of 100 or 110 minus your age. That has been modified by the U theory of 100 or 110 minus your age until retirement (basically 35% to 45% stock at retirement) to minimize the sequence-of-return risk. A market crash has its greatest impact in the first 10 years of retirement. It has moderate impact during the middle 10 years and minimal impact during the last 10 years. That is the data supporting the upper glide slope theory. The after retirement part of the U curve is basically the rising glide slope theory. Modern Portfolio Theory charts show the minimum risk portfolio as having around 35% stock. Risk is measured by standard deviations. Increasing the bond portion lowers return and increases risk. Increasing the stock portion increases returns and increases risk. Portfolios of 40-50% stock are moderately risky. Above 75% risk increases faster than returns. What does all this mean? The downward glide slope theory (100 or 110 minus your age) is fine I suppose but few people have any money to invest at the age of 25. At age 35, 100 or 110 minus age puts the young investor around 65-75% equity. I think 65% is a bit low because a young investor has another 30 years to ride out downturns before retiring. Using the upward glide slope depends on how active you think you will be in managing your portfolio when you become senile. If retiring at 65 then the first 10 years are 65-75, the mid-10 are 75-85, and the last 10 are 85-95. The upper glide slope and U theories are fine if you think you will still be actively managing your portfolio into your upper 80s and early 90s. Very few of us will be able to do that. All of these theories have a grain of truth as their basis. Since most people do not have investment money when young and won't be making investment decisions in their 90s I tend to believe something in the middle is more appropriate. Here is a table from Wade Pfau's 2018 update of the Trinity Study (1998) which verified Bengin's original research (1994). Success rates are for a 4% initial withdrawal, dollar withdrawals adjusted for inflation.

|---------- Payout Period----------|

Allocation 25 yr. 30 yr. 35 yr. 40 yr. 100% stock 99% 94% 91% 89% 75% stock 100% 98% 93% 92%

50% stock 100% 100% 97% 87% 25% stock 100% 87% 71% 45% 0% stock 79% 44% 28% 11% You need to be comfortable with how your portfolio is set up. That is different for everyone. I'm 73 and I'm setting up my portfolio so that it will stay around 60-65% equity regardless of age. |

|

|

|

Post by FD1000 on Nov 6, 2023 21:30:16 GMT

Mus: There are multiple theories. Bengen's research, as well as others, indicate that stocks should be as close to 75% as possible and never less than 50% for basically all withdrawal periods from 15 years to 40 years. The FIRE (Financial Independence Retire Early) investors believe that for early retirement stocks need to be 80% to support a longer payout period.

FD: most of investors of the above do not have enough money and/or retired way too early.

=========================

|---------- Payout Period----------|

Allocation 25 yr. 30 yr. 35 yr. 40 yr.

100% stock 99% 94% 91% 89%

75% stock 100% 98% 93% 92%

50% stock 100% 100% 97% 87%

25% stock 100% 87% 71% 45%

0% stock 79% 44% 28% 11%

FD: my conclusions and using a ball park %:

1) For someone who has a portfolio at 20-25 times their annual expense, and not including SS. The sweet spot is at 35-40% stocks.

2) For someone who has a portfolio at 25-35 times their annual expense, and not including SS. The sweet spot is at 25-35% stocks.

3) For someone who has a portfolio at 35-40+ times their annual expense, and not including SS. The sweet spot is at 15-100% stocks.

Without a pension: For someone who has a portfolio at under 15-20 times their annual expense = higher % in equity and suffer thru volatility and don't tell me it doesn't bother you.

|

|

|

|

Post by retiredat48 on Nov 7, 2023 1:04:35 GMT

My info from various retiree studies is that a 15/85 through 85/15 was about comparable in providing safety. Also meaning, a 100/0 or 0/100 was not optimal and more risky. Sort of consistent with Mustang's table above.

It's why I have been OK at times having a 72% stock side allocation, and during early COVID period a 50% stock side allocation.

Disclosure: I have used a HEDGE fund occasionally to remove some stock side exposure.

R48

|

|

|

|

Post by mozart522 on Nov 15, 2023 12:47:57 GMT

It seems like all the studies are based on 4% SWR, but that doesn't apply to everyone. If I have the same level of expenses, but twice the portfolio value, then I only need a 2% withdrawal rate and can have a much lower allocation to stocks. So a lot of it is just personal preference and one's individual situation. I have never adhered to any withdrawal rate, I just take what I need and my portfolio has continued to grow since retirement. I am rarely above 30% equities. There just is no right general answer. Also, I believe money managers and planners assume investors will be paying AUM fees, so need a higher stock allocation.

|

|

|

|

Post by Chahta on Nov 15, 2023 13:23:34 GMT

Another view is the "barbell" approach. Traditionally when stocks are up, bonds are down and vice versa. 50/50 may be the best for balancing income. Of course the last couple of years with inflation and aggressively rising rates 50/50 did not work as planned so a cash buffer is always best to keep for these times. 50/50 will work again once rates stabilize or start down.

|

|

|

|

Post by steelpony10 on Nov 15, 2023 13:45:28 GMT

The answer is whatever you want any way you want it because you’re dabbling with unknowns.

Now if you start believing you’ve perfectly predicted not projected your future that’s where you screw up. Studies just project in general terms and have little to do with personal goals, needs or circumstances.

Portfolio management demands you adapt as you go along to unknowns or you can fail based on lack of skill, luck and chance no matter what you do. That’s why one should settle on a long term plan. You’re dealing with random events where any plan is valid or can fail.

|

|

|

|

Post by richardsok on Nov 15, 2023 16:28:53 GMT

The answer is whatever you want any way you want it because you’re dabbling with unknowns. Now if you start believing you’ve perfectly predicted not projected your future that’s where you screw up. Studies just project in general terms and have little to do with personal goals, needs or circumstances. Portfolio management demands you adapt as you go along to unknowns or you can fail based on lack of skill, luck and chance no matter what you do. That’s why one should settle on a long term plan. You’re dealing with random events where any plan is valid or can fail. Um, yes. Nevertheless probabilities DO exist in the market. That's beyond question, pony. Some of us (FD, Harley and you-knw-who) attempt to identify and exploit them. I admire FD b/c he makes few new positions, but they are large ones. I confess I am suspicious of the high-wire indicator-patterns Harley makes use of -- but who are we to argue with success? He's good at it and he uses it. I'm not so I don't. Any good poker player will tell you to bet big when you uncover a 60-40 probability hand. You may very well lose such a hand, but that doesn't make the laws of probability less valid. When I see a fund that is steadily dropping in price, I instantly know that the odds are against me, so I avoid it, no matter what my market opinions. You are certainly correct that the technical investor is forever adapting to signals -- BUT while you may fail on any one trade, you will succeed over time if you consistently maintain yourself on the sunny side of probabilities. |

|

Deleted

Deleted Member

Posts: 0

|

Post by Deleted on Nov 15, 2023 17:45:06 GMT

Probabilities do exist in the market....

Annual SP500 will be up 82% of the time and down 18%.

SP500 average return in up years will be 18% and -16% in down years.

N=39

I am standing pat with these cards.

|

|

|

|

Post by Mustang on Nov 15, 2023 18:19:03 GMT

It seems like all the studies are based on 4% SWR, but that doesn't apply to everyone. If I have the same level of expenses, but twice the portfolio value, then I only need a 2% withdrawal rate and can have a much lower allocation to stocks. So a lot of it is just personal preference and one's individual situation. I have never adhered to any withdrawal rate, I just take what I need and my portfolio has continued to grow since retirement. I am rarely above 30% equities. There just is no right general answer. Also, I believe money managers and planners assume investors will be paying AUM fees, so need a higher stock allocation. You are correct. Based on a lot of research 4% is the maximum safe withdrawal rate based on the worst starting retirement date in history (1966). It is a draw down method. A method used when dividends and interest are not enough to pay the bills. Success is defined as not running out of money during the payout period.

Investors with sufficient funds would most likely select a different withdrawal method. I would imagine an income method (taking only dividend and interest) leaving principal untouched would be preferred. This method would change the composition of the investment toward dividend paying stocks and a heavier proportion of bonds.

An investor's asset allocation should be directly related to his withdrawal strategy.

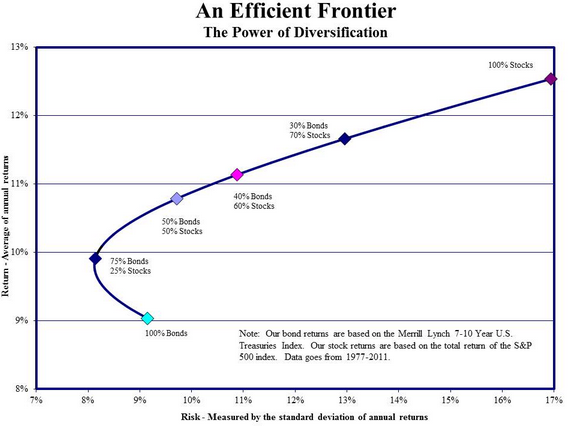

Edit: Modern Portfolio Theory has what is called an efficient frontier. It is the boundary showing the best return for the risk. It changes over time because investment returns vary. This chart is based on data from 1977-2011. Charts that include later data will show a different efficient frontier because bond returns were lower. On this chart the minimum risk portfolio is 25% stock and 75% bonds. Increasing the bond portion lowers returns and increases risk. Increasing the stock portion increases both returns and risk Risk increases faster as more stock is added. On this chart a 60/40 stock to bond asset allocation has balanced risk and return. An individual investor needs to balance needed return with acceptable risk (Sorry, I couldn't find a more up to date chart.)

Reminder: This particular curve is valid only for this data set. But it is representative of how MPT works.

|

|

|

|

Post by steelpony10 on Nov 15, 2023 18:44:21 GMT

richardsok , Ha. Ha. As long as we remember we are all anonymous posters with different motives. I’m just looking to be entertained, maybe find an unknown gem. Now that I believe my income is secure into the afterlife with a few restrictions I hope VTI becomes 90%+ of my portfolio someday because it’s purposed for LTC which I believe if left unrestricted is my best option long term. That’s where the subject of this post fails me and maybe others because if I ever followed any “conventional wisdom” throughout my investing life it would have been counter productive to my personal investing hopes and goals. Funny you mentioned poker. I’ve played a lot over my lifetime. My motive was to set players up for the kill shot which of course they were trying to do to me. I bet big one time with a full house and lost to a straight flush. Great favorable odds but it turned out to still be just a gamble no matter what “I thought”.

|

|

|

|

Post by yogibearbull on Nov 15, 2023 20:51:40 GMT

Mustang, while 1965 was among the worst start dates for withdrawal programs (but one problem is that free PV data goes back to 1985 only), 2000 was also quite BAD. There are related threads/posts nearby.

|

|

|

|

Post by mozart522 on Nov 15, 2023 21:39:43 GMT

Mustang, Not only will later data sets be different, but any period within the 34 years shown will likely be different. For example, the 5 year period between 2005-2010 would probably look much different. EF is interesting but not really actionable because it is only known after the fact and as you point out is not likely to repeat.

|

|

|

|

Post by FD1000 on Nov 16, 2023 0:09:11 GMT

It seems like all the studies are based on 4% SWR, but that doesn't apply to everyone. If I have the same level of expenses, but twice the portfolio value, then I only need a 2% withdrawal rate and can have a much lower allocation to stocks. So a lot of it is just personal preference and one's individual situation. I have never adhered to any withdrawal rate, I just take what I need and my portfolio has continued to grow since retirement. I am rarely above 30% equities. There just is no right general answer. Also, I believe money managers and planners assume investors will be paying AUM fees, so need a higher stock allocation. Bingo, if you have enough 30% max sounds about right to me, you can even go lower for long periods when markets are too volatile, or if you are a decent trader. My rules for most have been:The less you have, the more you must be in stocks and suffer the volatility. The more you have, the more options you have. Unfortunately, most Americans, fall within the first group, that's why there are so many discussions about it, and luck plays a big role with their retirement. Retiring in 2000 was much worse than 2010. It can get worse, many retirees start investing in single stocks and own many funds just to find out after 20 years, if they are honest, that a limited number of funds and hardly trading has been much better. |

|

|

|

Post by archer on Nov 16, 2023 0:23:51 GMT

Mustang , while 1965 was among the worst start dates for withdrawal programs (but one problem is that free PV data goes back to 1985 only), 2000 was also quite BAD. There are related threads/posts nearby. This calculator goes back further but doesn't allow specific funds like PV does. It does however let you plug in different allocations and withdrawal strategies. ficalc.app/ |

|

|

|

Post by mozart522 on Nov 16, 2023 12:26:05 GMT

It seems like all the studies are based on 4% SWR, but that doesn't apply to everyone. If I have the same level of expenses, but twice the portfolio value, then I only need a 2% withdrawal rate and can have a much lower allocation to stocks. So a lot of it is just personal preference and one's individual situation. I have never adhered to any withdrawal rate, I just take what I need and my portfolio has continued to grow since retirement. I am rarely above 30% equities. There just is no right general answer. Also, I believe money managers and planners assume investors will be paying AUM fees, so need a higher stock allocation. Bingo, if you have enough 30% max sounds about right to me, you can even go lower for long periods when markets are too volatile, or if you are a decent trader. My rules for most have been:The less you have, the more you must be in stocks and suffer the volatility. The more you have, the more options you have. Unfortunately, most Americans, fall within the first group, that's why there are so many discussions about it, and luck plays a big role with their retirement. Retiring in 2000 was much worse than 2010. It can get worse, many retirees start investing in single stocks and own many funds just to find out after 20 years, if they are honest, that a limited number of funds and hardly trading has been much better. One of the options that having more than you need is you can eliminate FOMO (fear of missing out). I am heavily in cash right now, happy with the 5+%. Yes, in hindsight 500 index would have done better over this year, but I'm still above where I was in January. That is really my only benchmark. I enjoy your posts, FD. |

|

|

|

Post by johntaylor on Nov 19, 2023 14:55:20 GMT

Lot of different views on this, but Ellis noted that one's actual time horizon might be that of a child or charity and concluded "...don't change your investments just because you have reached a certain age or have retired" (Winning the Loser's Game, Fifth Ed, 142-143)

|

|

|

|

Post by retiredat48 on Nov 19, 2023 15:18:39 GMT

Lot of different views on this, but Ellis noted that one's actual time horizon might be that of a child or charity and concluded "...don't change your investments just because you have reached a certain age or have retired" ( Winning the Loser's Game, Fifth Ed, 142-143) ,................... .+1Yes indeed...I agree with the author. When you have enough, invest as though it is your heir's investment allocation. And if no children, and perhaps a college, realize they have very large stock allocation percentages. Further, I do not understand those who say that if you get a larger portfolio, and need to take a lesser percent in RMDs to live on, that you should keep reducing your equity allocation side? You likely got this higher valuation due to stock/fund price rises over time. Let it ride. The increased dollar value provides a buffer against any market decline. And stocks in the long run beat bonds. Lastly, I have posted often: "When you have your first million, (or enough), the goal is not to make the second million; rather it is to hedge the first million and protect it." So you strategically build a portfolio to hedge things. Such as, inflation a huge threat?? Own stock funds and perhaps some oil based companies...or real estate (I have three homes, clearly a "second million" hedge). Growth stocks way pricey by historical standards?? (Think magnificent seven), balance with some value stocks and small caps. Interest rates taken to zero for a decade? shorten fixed income durations and invest in dividend paying alternatives, such as income builder funds, preferred stock funds, FI CEFs. Government needs to finance huge debts with interest rates rising (like now!), increase FI durations and lock in some good rates long term; use bond ladders to your advantage, rollover into higher and higher rates if that occurs. And so on... R48 |

|

|

|

Post by FD1000 on Nov 19, 2023 15:23:16 GMT

Mustang , while 1965 was among the worst start dates for withdrawal programs (but one problem is that free PV data goes back to 1985 only), 2000 was also quite BAD. There are related threads/posts nearby. This calculator goes back further but doesn't allow specific funds like PV does. It does however let you plug in different allocations and withdrawal strategies. ficalc.app/Wow, I used the above calculator with 10/90(stocks/bonds) and withdrawal of $20K = 2%(we need less than 2%) of one million portfolio. Success rate =100% |

|

|

|

Post by gman57 on Nov 19, 2023 15:32:54 GMT

Mustang , while 1965 was among the worst start dates for withdrawal programs (but one problem is that free PV data goes back to 1985 only), 2000 was also quite BAD. There are related threads/posts nearby. I retired mid-2007 -- 2008 and early 2009 wasn't exactly a picnic time to retire either. I lost a boat load during that time right after I retired...ouch. |

|

|

|

Post by yogibearbull on Nov 19, 2023 15:48:33 GMT

|

|

|

|

Post by gman57 on Nov 19, 2023 16:02:52 GMT

I don't pay attention to withdrawal rate strategies. Life is too non-linear. Major illnesses or especially LTC (long term care) and you can throw withdrawal rates out the window IMHO. |

|

|

|

Post by Chahta on Nov 19, 2023 16:03:29 GMT

gman57 , I am not sure why retirees do not universally have a cash buffer to help sidestep bad markets. It just seems the prudent thing to do. This should be done in pre-retirement planning. I do not know if you did or didn't. I read about so many retirees experiencing Sequence Risk.

|

|

|

|

Post by gman57 on Nov 19, 2023 16:09:09 GMT

gman57 , I am not sure why retirees do not universally have a cash buffer to help sidestep bad markets. It just seems the prudent thing to do. This should be done in pre-retirement planning. I do not know if you did or didn't. I read about so many retirees experiencing Sequence Risk. I had "safe money" to get by 2008-2009 without selling anything but even if you have the cash it makes you think... this isn't fun. It makes you reassess your asset allocation/risk tolerance. |

|

|

|

Post by mozart522 on Nov 19, 2023 16:13:20 GMT

Lot of different views on this, but Ellis noted that one's actual time horizon might be that of a child or charity and concluded "...don't change your investments just because you have reached a certain age or have retired" ( Winning the Loser's Game, Fifth Ed, 142-143) ,................... .+1Yes indeed...I agree with the author. When you have enough, invest as though it is your heir's investment allocation. And if no children, and perhaps a college, realize they have very large stock allocation percentages. Further, I do not understand those who say that if you get a larger portfolio, and need to take a lesser percent in RMDs to live on, that you should keep reducing your equity allocation side? You likely got this higher valuation due to stock/fund price rises over time. Let it ride. The increased dollar value provides a buffer against any market decline. And stocks in the long run beat bonds. Lastly, I have posted often: "When you have your first million, (or enough), the goal is not to make the second million; rather it is to hedge the first million and protect it." So you strategically build a portfolio to hedge things. Such as, inflation a huge threat?? Own stock funds and perhaps some oil based companies...or real estate (I have three homes, clearly a "second million" hedge). Growth stocks way pricey by historical standards?? (Think magnificent seven), balance with some value stocks and small caps. Interest rates taken to zero for a decade? shorten fixed income durations and invest in dividend paying alternatives, such as income builder funds, preferred stock funds, FI CEFs. Government needs to finance huge debts with interest rates rising (like now!), increase FI durations and lock in some good rates long term; use bond ladders to your advantage, rollover into higher and higher rates if that occurs. And so on... R48 Meanwhile, Dr. Bill Bernstein says “When you've won the game, stop playing.” What he meant by that is you need to take risk to accumulate a nest egg for retirement (play the game), but once you've reach your goal (won the game) you should attempt to reduce investment risk as much as possible (stop playing)." I agree with Bill. De-risking means I know that I'll be good and that my heirs will get a nice pile. |

|

|

|

Post by Chahta on Nov 19, 2023 16:16:13 GMT

gman57 , I am not sure why retirees do not universally have a cash buffer to help sidestep bad markets. It just seems the prudent thing to do. This should be done in pre-retirement planning. I do not know if you did or didn't. I read about so many retirees experiencing Sequence Risk. I had "safe money" to get by 2008-2009 without selling anything but even if you have the cash it makes you think... this isn't fun. It makes you reassess your asset allocation/risk tolerance. I agree 100%. But I have never worried about drawdowns so much. They made me angry not scared. And owning interest/div paying assets makes it a little better. The payoff this time will be the first interest rate reduction by the Feds. |

|

|

|

Post by Chahta on Nov 19, 2023 16:18:14 GMT

johntaylor ,................... .+1Yes indeed...I agree with the author. When you have enough, invest as though it is your heir's investment allocation. And if no children, and perhaps a college, realize they have very large stock allocation percentages. Further, I do not understand those who say that if you get a larger portfolio, and need to take a lesser percent in RMDs to live on, that you should keep reducing your equity allocation side? You likely got this higher valuation due to stock/fund price rises over time. Let it ride. The increased dollar value provides a buffer against any market decline. And stocks in the long run beat bonds. Lastly, I have posted often: "When you have your first million, (or enough), the goal is not to make the second million; rather it is to hedge the first million and protect it." So you strategically build a portfolio to hedge things. Such as, inflation a huge threat?? Own stock funds and perhaps some oil based companies...or real estate (I have three homes, clearly a "second million" hedge). Growth stocks way pricey by historical standards?? (Think magnificent seven), balance with some value stocks and small caps. Interest rates taken to zero for a decade? shorten fixed income durations and invest in dividend paying alternatives, such as income builder funds, preferred stock funds, FI CEFs. Government needs to finance huge debts with interest rates rising (like now!), increase FI durations and lock in some good rates long term; use bond ladders to your advantage, rollover into higher and higher rates if that occurs. And so on... R48 Meanwhile, Dr. Bill Bernstein says “When you've won the game, stop playing.” What he meant by that is you need to take risk to accumulate a nest egg for retirement (play the game), but once you've reach your goal (won the game) you should attempt to reduce investment risk as much as possible (stop playing)." I agree with Bill. De-risking means I know that I'll be good and that my heirs will get a nice pile. LOL....where you been? Today's million is two million. |

|